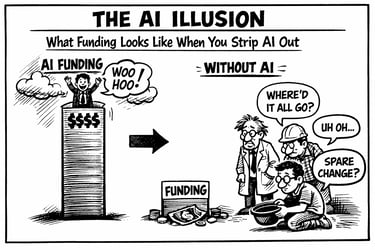

The AI Illusion: What Funding Looks Like When You Strip AI Out

The rise of artificial intelligence has not just reshaped venture capital it has distorted how we read it.

Mahalaxmi Ravichandran Vijayakumari

4/4/20265 min read

In 2026, venture capital seems to be making a healthy rebirth. Following the extreme contraction of 2022-2024, the overall amounts of funds raised by the globe are on the rise, a number of mega-rounds are increasing, and investors are no longer in survival mode but in cautious optimism. The news about rebound is being glorified with headlines that show the growth in the value of deals and the new momentum in the field of tech infrastructure. However, this is only a superficial recovery, a recovery that has been brought into being to almost a hundred percent by artificial intelligence.

As soon as you take away AI in the formula, the image becomes even darker. Non-AI industries are not only catching up, but several of them are stagnating or even shrinking, showing that the venture ecosystem has been much slimmer and weaker than the aggregate of it. It is not some sort of noise on a cycle. It is a restructuring of capital which hides the hidden frailty in the wider startup environment.

The Headline Recovery--and its Fallacy.

The zero-interest-rate policies and SPAC mania reached their peak in 2021, making Global VC take off. Then reality set in: the 2022 deal values were down 35-40 per cent at rates spiking and valuations reset. The pain was later continued in 2023 and 2024 when dry powder remained idle and founders were cutting burn rates to lengthen runways.

By 2025 life was showing, total investment was nearly 366-490 billion. Current trends are confirmed, with AI-powered infrastructure (chips, compute clusters) and foundation models leading to mega-deals in the early 2026. In theory, it is a classic recovery curve: capital returns, risk appetite is increasing, ecosystem flourishes.

The fallacy is in aggregates. As mentioned in the script of analysis in question, averages are misleading in the scenario when there is a skew in the distribution. Suppose a room full of people that made 30,000 each year, until a billionaire enters. The average wage increases tremendously, but does not inform you about the average laborer. VC data is no exception: a single prevailing industry carries the headline covering stagnation in other areas.

AI's Meteoric and Concentrated Rise

AI was not only involved in the rebound, but it wrote the book. By 2023, AI had taken 15-20 percent of the global VC, which was approximately $55-70 billion, following the ChatGPT boom. By 2024, investments grew to almost twice the amount of up to 100-130 billion (30-35% share) since AI was the only story. Then 2025 became the point of turning point: AI raised 190-225 billion, or 52-63% of all VC - the first time that it crossed the 50% line.

By 2023-2025, AI alone will have captured close to 345-355 billion of the total VC deployed of one point trillion or one point one trillion. It is a third in all the money going to one industry in three years. The current reports indicate that in 2026, AI will own majority share via infrastructure and chip mega-rounds, but the number of deals is not increasing accordingly, which implies that there are fewer startups that will get significantly larger checks.

AI Out of the AI In: Stagnation Unveiled

The non-AI funding is even a worse story. In 2023, it comprised $280-320 billion. This reduced to $198-260 billion by 2024 with AI consuming an increasing portion of a declining pie. By 2025, non-AI investments were flat to slightly decreasing to $176-295 billion - some estimates indicate that the decrease was 10 percent even though the total VC is increasing.

Consumer technology, fintech, marketplace and SaaS are not going back to 2021 heights. Multiples are still at 5-8x as compared to 2021 and 15-20x; founders declare wary LPs. It is the ecological fallacy in its full flower, the boom in this sector raises the average, deceiving us to think it was in health.

Lessons on Market Breadth Public Markets

Steal an idea equities: market breadth. The recent S&P 500 rallies were spectacular on Magnificent 7 strength (Nvidia, Apple, etc.), and hundreds of stocks under the index were flattened or decreased. The news was trumpeting that it was a bull market; concentration was being shown by breadth.

VC is currently following this trend. The overall volume is increasing, but the breadth is getting worse -capital is concentrated in AI and the traditional industries are in the headwinds:

Fintech: Tougher rules, downward growth since 2021 frenzy.

Consumer: Soft demand, high cost of customer acquisition.

SaaS: Multiple is going to be low, and not going back to a frothy multiple.

Capital flows are rational into the perceived best returns and this brings about instability.

The Mega-Round Deep Dive Paradox

Mega-rounds help in accelerating concentration. Fourteen companies took up 41 percent of the total of VC dollars in H1 2025 alone. These are not seed-level scrapers: they are billion-dollar monopolies:

OpenAI: 4B raise, which is more akin to a research institute -non-profit dynamics and limitless capital needs.

Anthropic: $800M Series C after biotech-type dilution lines (slow profitability curves)

Scale AI: $200M Series D, services-intensive (data labeling/evaluation) with multiples of SaaS instead of 100x venture upside.

The contradiction: The screams are of success (500M Series C! 10B+ valuations!), which is an indicator of domination and momentum. However, they limit the upside of investors. Even 10x exits would be mundane in the power-law world of VC that requires 100x+ unicorns to make returns on a fund-level basis. Bigger checks imply a reduced ownership, and squeegee potential multiples.

There are four fundamental risks that are increased by concentration:

Compute Costs: Existing estimates believe that there is a small, high-priced GPUs that will offer long-lasting moats. However, costs (Nvidia roadmaps, custom silicon) might be reduced 70-80 percent in two years, and scarcity-based advantages will be undermined.

Onslaught to Open Source: Models such as Llama and Mixtral can narrow performance disparities to proprietary LLMs in a short period of time, fast, free, and good enough. This commoditizes the advantage that makes the difference in the valuations of up to 2B dollars.

Revenue Reality Check: The speed with which capital is deployed prior to revenue curves is warp speed. In case ARR growth does not keep up with the deployment rate, valuation multiples squeeze throughout the concentrated theme.

Power-Law Fragility: VC is a company based on dispersed bets in terms of innovation cycles and industries. AI correlation converts the diversified portfolios into the de facto one-theme funds. Everything is struck simultaneously by a sentiment change.

Steeleman: Why Bulls Could Be Right

The counterarguments to fairness are:

Platform Shift, Not Hype Cycle: As in the case of cloud computing in 2010 (first turbulence to trillions of dollars), AI may become fundamental. First mover advantage is intelligent positioning.

Spillover Effects: AI cuts expenses in industries -fintech underwriting, biotech discovery, consumer operations. The non-AI breadth can be an outcome of sequencing.

Sustainable Moats: There could be multiples of data flywheels, enterprise entrenchment, and workflow embedding. Amazon seemed overvalued over ten years; real winners prove to be right with time.

The Decree: Half Recovery, Half Care.

AI backlash Venture capital is coming back. Hard-selling, persuasively, with enormous commitment and investment of funds. Everywhere else? The ecosystem is stagnant, homogenous and susceptible.

The only way to recover is comprehensively: various sectors, phases, and regions developing simultaneously. Monitor that above others, but not headline volume. During the upswing, it is thrilling with concentration, during corrections, it haunts. AI illusion lives as long as you are willing to take it off and reveal the truth behind it.